Professional traders use logic and math to design strategies, and Average True Range (ATR) is a critical component. Traders often use ATR to boost profit projection as well as define risk.

It is imperative to identify benchmark ranges (ATRs). This vertical indicator (high minus low) may reveal when a market has reached overbought or oversold status. It is also used to gauge when a market has consolidated enough, thus favoring a breakout or onset of a trend. Vertical measurements are speedometers.

Speed Matters

When is the speed of a rally or decline too quick? There are many indicators that were created to signify when a market is overbought or oversold. RSIs and stochastics are probably the most popular technical gauges for speed. Moving Average Convergence Diversion (MACD) is a widespread pace indicator too.

Vertical and Horizontal Dimensions

During the MTM Daily Edge sessions each afternoon, we track momentum and/or directional bias and speed for stocks, ETFs and futures. The combination of speed and direction are integral elements when designing strategy. Opportunities rise when the speed of a move is well above the norm or when day ranges and volume are far below average.

Too Fast, Think Theta

If a day range spans 175% of the benchmark ATR, it is thought to have traveled too far and fast. Thus, odds favor 2 to 3 days of sideways trade where time decay (theta) becomes the dominant factor. Premium decays when prices stagnate. Another situation where theta pays is when a market moves the length of an average week over a 48-hour period. When this occurs a 3-to-5-day consolidation phase often follows.

Too Slow, Play Direction

After a couple of weeks where the day ranges have been below the average, odds increase for a breakout or onset of a trend. Under these circumstances, long puts and bearish spreads should pay when a major support level is violated. Or long calls should pay if a critical resistance area is breached.

Use ATR to Project Profit and Manage Risk

Once a trend begins, traders want to know how long the move will last, both in time and distance. I frequently use ATR to set targets over various time frames. For example, say a market has had similar and below average ranges for a five-day stretch. Assume the market broke through resistance. When a breakout signal is realized, the first target (T1) is the length of an average day. When T1 is reached, move risk (stop loss) to cost. With this strategy you will scratch the trade for no loss if the trend does not materialize. If the trend continues to extend, set the second target (T2) at the length of average week range from entry. When that price trades, risk goes to T1.

Using this method, one may lock in profits as the trend extends. Each market has its own traits, and this management technique is ideal for locking in profits as the trend extends.

Preferred ATRs for Comparison

The ATRs I prefer for comparisons are as follows:

- 14 days

- 9 weeks

- 7 months

- 5 quarters

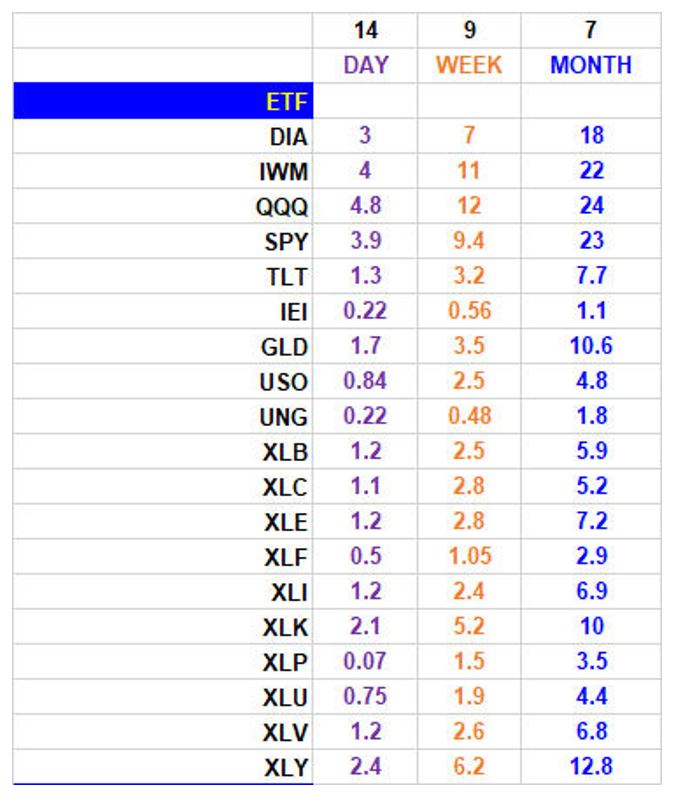

ATRs for Popular ETFs

Find time for research to create your own spreadsheet of average ranges of your favorite stocks or commodities. A good trader prepares and has pertinent data available to set risk and targets immediately after a position has been entered. To get you started I’ve included a spreadsheet of Average True Ranges for some of the most popular ETFs below.

John Seguin

Senior Technical Analyst

Market Taker Mentoring, Inc.